When private equity takes control, managers face a stark reality: create value fast or become a cost to be cut. Konstantinos, Marie-Amelie, Matilda, Rebecca and Xiangyu argue that private equity replaces comfort with discipline and accountability. Through the case studies of Toys “R” Us and Hilton, they reveal it is leadership response – not financial pressure – that determines outcomes.

Private equity (PE) ownership involves a trade-off: capital for control. When PE takes control, the management comfort zone evaporates. Board meetings shift from passive reviews to intense strategic engines. Intuition is replaced by data-driven precision, and managers must master unit economics and EBITDA (earnings before interest, taxes, depreciation, and amortisation) margins as survival metrics amid financial leverage.

Ultimately, PE ownership compresses decades of organisational change into a few years. PE sponsors accelerate transformation by realigning incentives, offering equity stakes that turn managers from employees into partners with skin in the game. Strategic decisions, from cost-cutting to mergers and acquisitions are engineered around one objective: expanding valuation multiples before time runs out. A culture of radical accountability is created, in which management is no longer simply running a business but executing a high-stakes investment thesis in which hitting the metrics determines who stays and who goes.

We explore what happens when PE ownership meets management reality. Through the contrasting cases of Toys “R” Us and Hilton, we illustrate how PE ownership turns management into a sink-or-swim environment: managers must create value quickly, or risk being cut from the plan altogether.

Why Toys “R” Us management failed under PE

The collapse of Toys “R” Us illustrates what happens when management fails to adapt to the pace of change imposed by PE ownership. After the 2005 leveraged buyout, the company carried roughly $7.6 billion in debt and spent around $400 million annually servicing it. Instead of using this constraint as a catalyst for reinvention, leadership prioritised short-term financial survival over strategic investment.

Management focused on preserving the existing business rather than transforming it. Investments in e-commerce, store modernisation, and digital capabilities were delayed, while competitors like Amazon accelerated.

The failure was not simply the presence of debt, but how management responded to it. Leadership prioritised servicing obligations over the innovation and transformation needed to remain competitive.

Strategic adaptation at Hilton

If Toys “R” Us illustrates managerial inertia, Hilton shows what happens when leadership embraces the transformation demanded by PE ownership. Blackstone acquired Hilton for $26 billion in 2007, just before the global financial crisis forced a 70% write-down of its equity investment. Yet by 2018, the deal had generated $14 billion in profit, becoming one of the most successful leveraged buyouts in history.

The difference lay in how management responded. Hilton’s leadership implemented sweeping operational change, restructuring corporate operations, and shifting the company toward an asset-light model based on franchise and management contracts. This dramatically improved capital efficiency and enabled rapid global expansion.

PE governance also made leadership accountability explicit. Blackstone installed Christopher Nassetta as CEO early in the investment, signalling that management roles depended on executing the transformation. By aligning incentives with equity and delivering operational improvements, Hilton’s management became a driver of value creation rather than a constraint.

Why managers sink or swim: A resistance to change framework

Why did Hilton adapt under PE while Toys “R” Us unravelled? The difference was not simply the investment plan, but how management responded to the organisational change PE imposed.

Organisational change research shows that major transformations reliably trigger resistance from the very people expected to deliver them. Resistance is most likely when change threatens autonomy, disrupts established routines, and creates uncertainty about future roles. PE does all three simultaneously: decision-making tightens, legacy practices are challenged, and management is suddenly held to a far more demanding performance regime.

This helps explain the contrast between the two cases. At Toys “R” Us, management responded defensively, prioritising short-term stability over reinvention. At Hilton, leadership embraced restructuring and became an active driver of change.

Studies argue that responses to change typically take four forms: voice, loyalty, neglect, or exit. In a PE-backed firm, voice can strengthen execution, but neglect is especially dangerous because delay quickly becomes missed targets and lost value.

When ownership changes: How managers can lead transformation

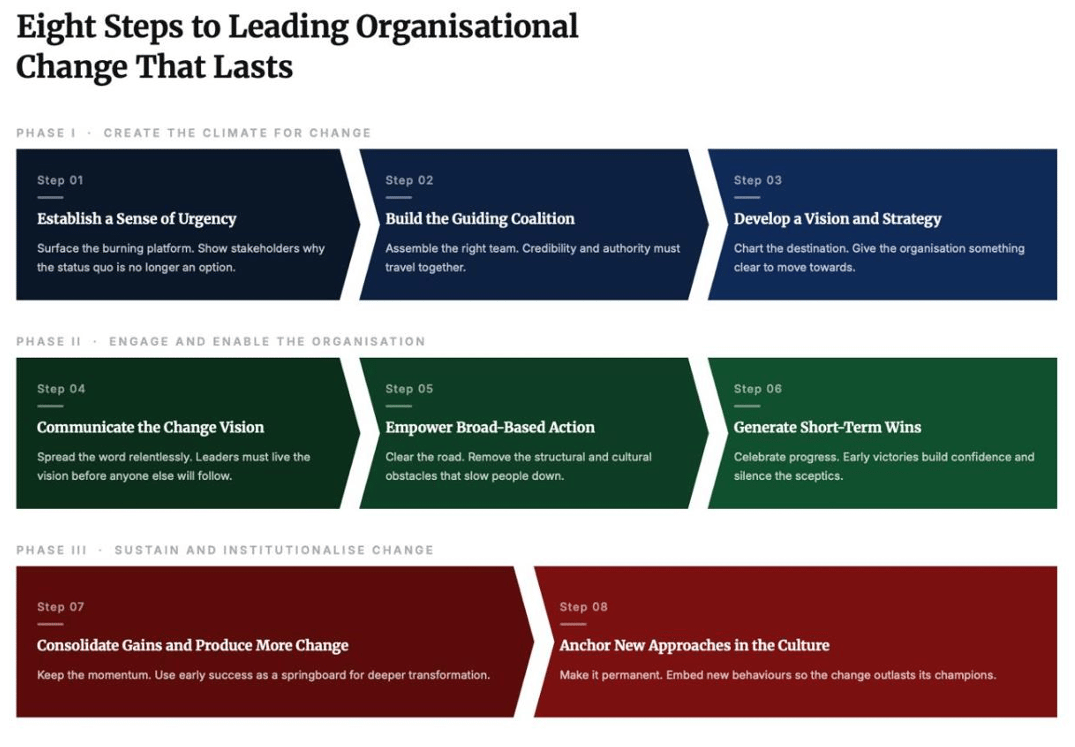

The question then becomes not simply why managers fail during ownership transitions, but what successful ones do differently. John P. Kotter’s framework (1996) of organisational transformation offers a useful guide:

First, managers must create a credible sense of urgency, explaining why existing practices cannot continue under the organisation’s new financial and competitive conditions. Second, they must build a guiding coalition by aligning influential leaders across key functions to support the transformation. Finally, they must translate ownership objectives into a clear vision and strategy that teams can understand and act upon.

Kotter’s framework continues to be widely applied in studies of organisational transformation across industries, such as in Sittrop and Crosthwaite (2021), Graves et al. (2023), and Mouazen (2024). Its continued relevance reflects that successful change requires managers to anticipate resistance and actively lead the transformations demanded by PE ownership.

Our takeaways

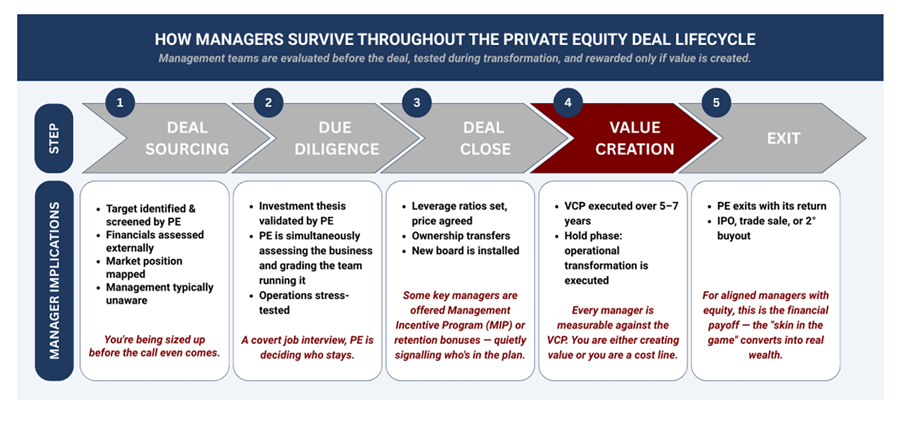

The contrast between Toys “R” Us and Hilton shows how differently management teams respond when PE ownership forces transformation. For managers entering a PE environment, the lesson is straightforward: ownership change demands leadership change. We therefore leave you with the PE deal lifecycle below. It captures the reality managers face under PE ownership: they are evaluated before the acquisition, tested during operational change, and rewarded only if value is created. Under PE ownership, leaders must actively drive transformation, or risk becoming part of the cost base.

- This blog was written by students undertaking a Global Master’s in Management degree at LSE’s Department of Management as part of the MG448A Capstone Course – Management in Action.

- This blog post represents the views of its author(s), not the position of the London School of Economics and Political Science Department of Management.

- Photo by Vitaly Gariev on Unsplash

The post When private equity takes control: Managers must create value or become a cost first appeared on LSE Management.